Apr 25, 2022

Category:

Buying, First Home

Calgary Mortgage Rates Explored: What’s a Good Mortgage Rate?

Mortgage rates in Calgary have been dropping to historical lows since the start of the pandemic. Before the pandemic, the average mortgage rates were around 8%. But at the start of 2021, these were only around the 2% range.

With the economy starting to recover, mortgage rates are now on the rise. And this trend is expected to continue throughout the rest of 2022. While current mortgage rates in Calgary are still considered low, they’re already increasing little by little.

If you’re planning to buy a home in Calgary, it’s better to lock in your home loan as soon as you can before the rates go further up. But first things first, what’s a good mortgage rate?

Header image source: Pixabay

What’s a Good Mortgage Rate?

The current mortgage rates in Calgary are around 4%. But it could always be higher or lower than that, depending on your situation and which lender you go for.

The main factor that influences mortgage rates is your financial situation. Lenders look into your credit score when you apply for a mortgage or preapproval. People with high credit scores usually get lower interest rates.

Lenders also look into your income situation. You should be able to prove that you have a stable source of income to get better rates.

There’s also the debt-to-income (DTI) ratio. This looks into how much of your monthly income is spent on paying off existing debts. A lower DTI ratio means a better financial standing.

The down payment you put on your home also affects your mortgage rates. The higher your down payment is, the lower your interest rate will be.

The lifespan of your loan is also another factor that comes into play. Shorter loan payment terms mean lower interest rates. But they also mean you’ll have to pay larger monthly amortizations.

There’s no one “good” mortgage rate as it differs for every person. You may want to consult with mortgage brokers in Calgary to get a better idea of the mortgage rates you can expect to get. Or you could always try a mortgage calculator for free.

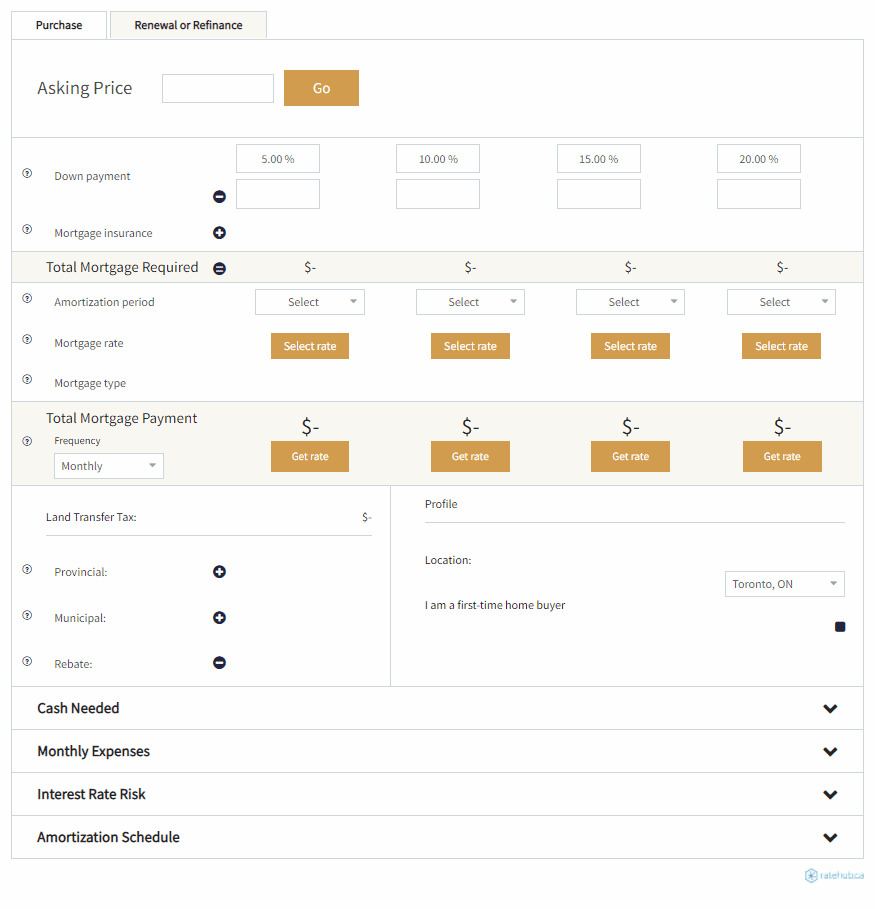

Mortgage Calculator

A mortgage calculator is a free online resource that you can use to see an estimate of your mortgage rates. It gives you a clearer picture of what you can expect to pay when you apply for a mortgage.

Here’s a simple and beginner-friendly mortgage calculator you might want to use.

The rate will be more accurate if you input more specific values. But remember that this mortgage calculator only serves as a guide. The rates you get may be close to the actual rate, but it won’t be able to give you the exact value.

Tips for Getting the Best Mortgage Rates

Check out these tips that might be helpful as you look for the best mortgage rates.

Apply to Different Lenders

The only way to get accurate loan estimates is to actually apply for a mortgage. Lenders have different rates and fees to offer. Some of them may even be able to give you a discount.

After getting a loan estimate, compare the values from different lenders. Pay attention to the interest rate and the annual percentage rate (APR). An APR contains all your borrowing costs, the interest rate, and other loan-related fees. It’s a more accurate value of what you’ll be paying monthly for the life of your loan.

Negotiate Rates and Terms

You can always try to negotiate mortgage rates with your lender. See if they can give you a discount or lower the interest rate by a bit more. See if you can get better terms, too.

Just because a lender offers the lowest rate doesn’t mean you should automatically go with them. If there’s a lender that offers better loan terms, you can show them the lowest offer and ask if they can match it.

Buy Discount Points

If you have some extra money, you may also want to avail discount points for your loan. One discount point is equal to 1% of the total loan amount. So, if you’re applying for a $500,000 loan, one discount point costs $5,000.

Generally, this could reduce your interest rate by 0.25%. If your current mortgage rate sits at 4.5%, buying one discount point could reduce it to 4.25%. That’s already a big saving for your loan.

Just keep in mind that discount points are paid upfront. You should be ready to pay it on closing day.

Discount points are great, but only avail these if you plan to stay in the house for a long time. Otherwise, it wouldn’t be such a practical investment.

Prepare for Your Mortgage Application

Even before buying a home—let alone applying for a mortgage preapproval—you should be well-prepared.

Try to increase your credit score by paying off some of your current debts. By doing so, you’ll have a better financial standing and a better chance of having lower interest rates.

If you can, try to save more for your down payment. This is the most effective way to lower your mortgage rates. A bigger down payment also means a smaller loan amount, and possibly, even a shorter lifespan for your loan.

Buying a Home in Calgary

Image source: Brenda Coulter

Calgary house prices are now on the rise due to the high demand and low housing supply. But overall, the Calgary real estate market is still worth buying into. Current mortgage rates are lower than normal. They’re nothing like the 2021 rates, but they’re still considered good.

If you’re interested in buying a home in Calgary, get in touch with a real estate agent to explore your options in the market. The earlier you lock in your mortgage rates, the more valuable your investment will be.

Again, here are some tips for getting the best mortgage rates in Calgary:

- Submit a mortgage application to different lenders.

- Compare the loan estimates and the terms.

- Negotiate with lenders to try and get lower rates and/or better terms.

- If you can, buy discount points to reduce your interest rate for the mortgage.

- Increase your credit score by paying off existing debts.

- Save up for a larger down payment amount so that you can have a smaller loan amount.

Written By